26 IS-LM model

Students will be able to:

- Understand the power of fiscal and monetary policy in a general equilibrium.

- Describe how the IS-LM model explains the interaction of real goods markets and financial markets in balancing interest rates and total output in an economy.

- Explain how investment acts as the key channel through which changes in real interest rates affect GDP in the short run.

- Recognize how the government or central bank can increase aggregate demand to combat economic downturns and crises.

Required readings:

Blanchard & Johnson (2013, ch. 5).

26.1 Putting the IS and the LM relations together

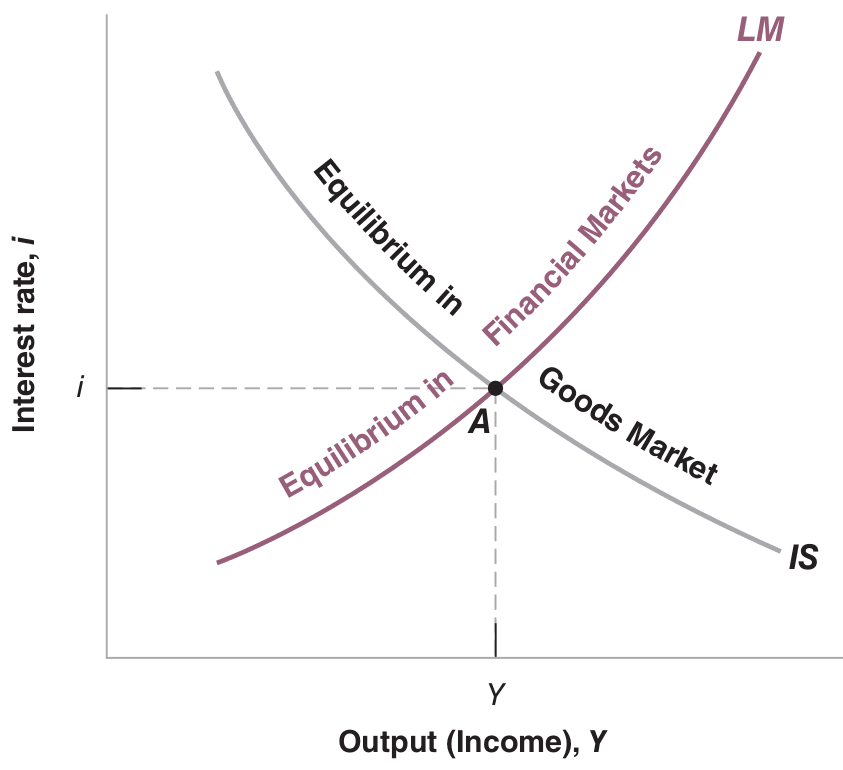

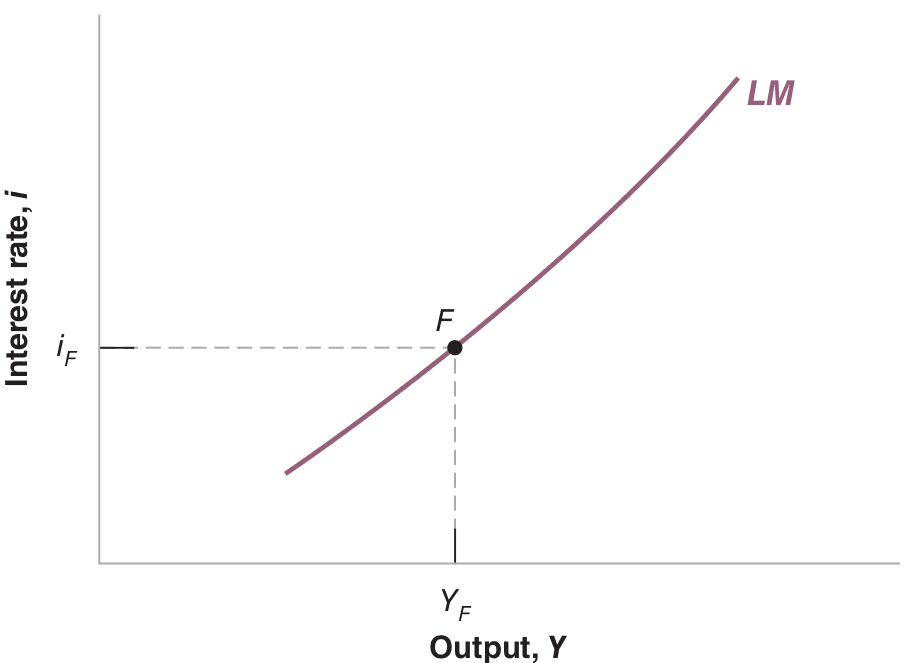

The IS relation stems from the condition that the supply of goods must equal the demand for goods, revealing how the interest rate affects output. Conversely, the LM relation stems from the condition that the supply of money must equal the demand for money, illustrating how output affects the interest rate. Now, by putting IS and LM relations together, we understand that at any time, both the supply of goods must equal the demand for goods, and the supply of money must equal the demand for money—both relations must hold. Together, they determine output and the interest rate.

The equilibrium in the goods market shows an interest rate increase leads to a decrease in output, depicted by the IS curve in Figure .

\[ \text{IS relation:} \quad C(Y-T) + I(Y,i) + G \]

The equilibrium in financial markets implies an output increase leads to an interest rate increase, represented by the LM curve in Figure .

\[ \text{LM relation:} \quad \frac{M}{P} = YL(i) \]

The IS-LM model is visualized in Figure 26.1. Only at point A, where both curves intersect, are goods and financial markets in equilibrium.

Note: Blanchard & Johnson (2013, p. 93)

You’ll notice the LM relation is expressed in real terms—relating real money (money in terms of goods), real income (income in terms of goods), and the interest rate. Remember: nominal GDP equals Real GDP times the GDP deflator: \(\$Y = Y \cdot P\). Conversely, Real GDP equals nominal GDP divided by the GDP deflator: \(\frac{\$Y}{P} = Y\).

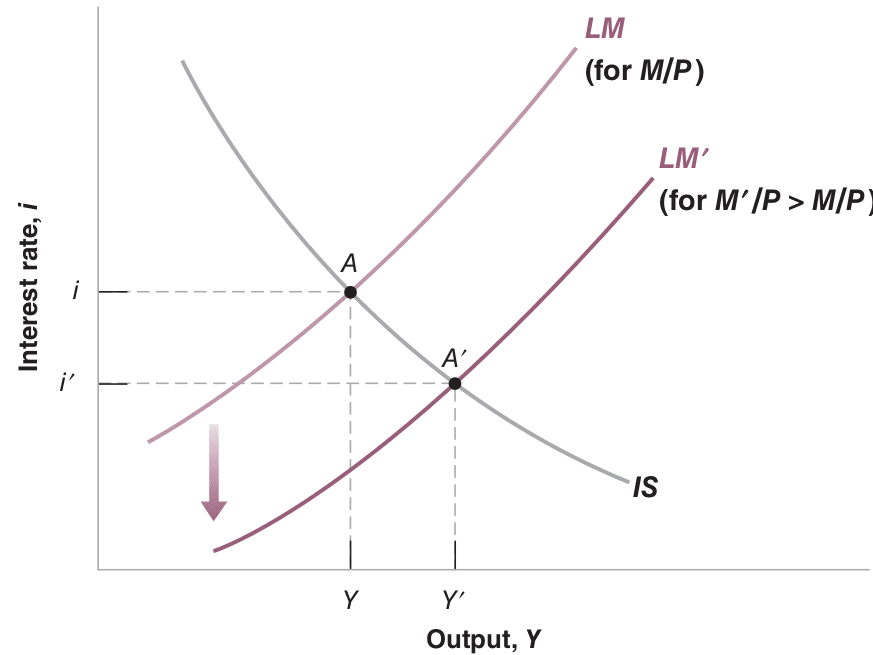

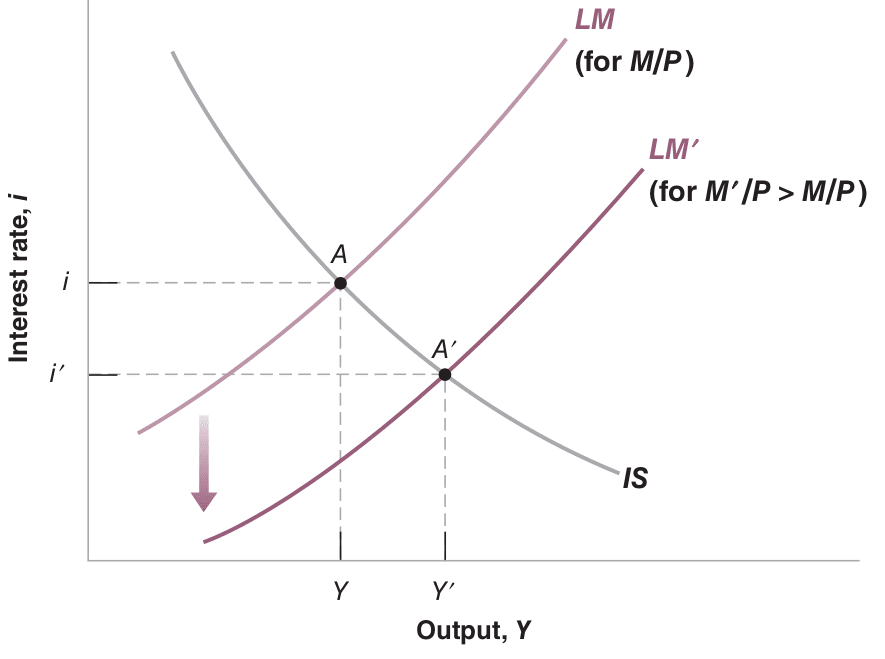

26.2 Monetary policy

A monetary expansion results in higher output and lower interest rates. Conversely, the reverse holds for a monetary contraction. See Figure Figure 26.2.

Note: Blanchard & Johnson (2013, p. 97)

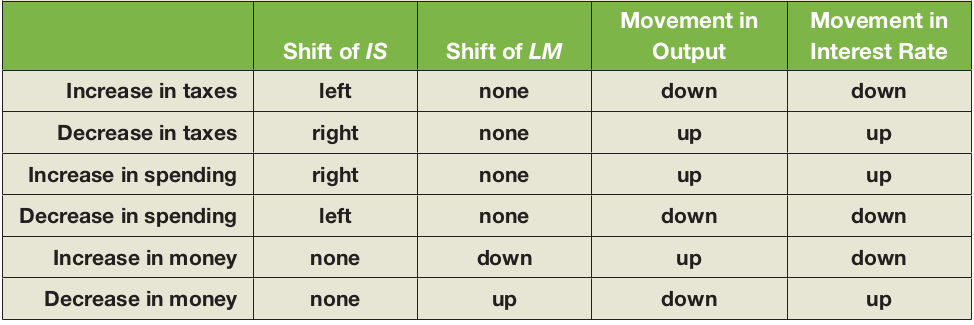

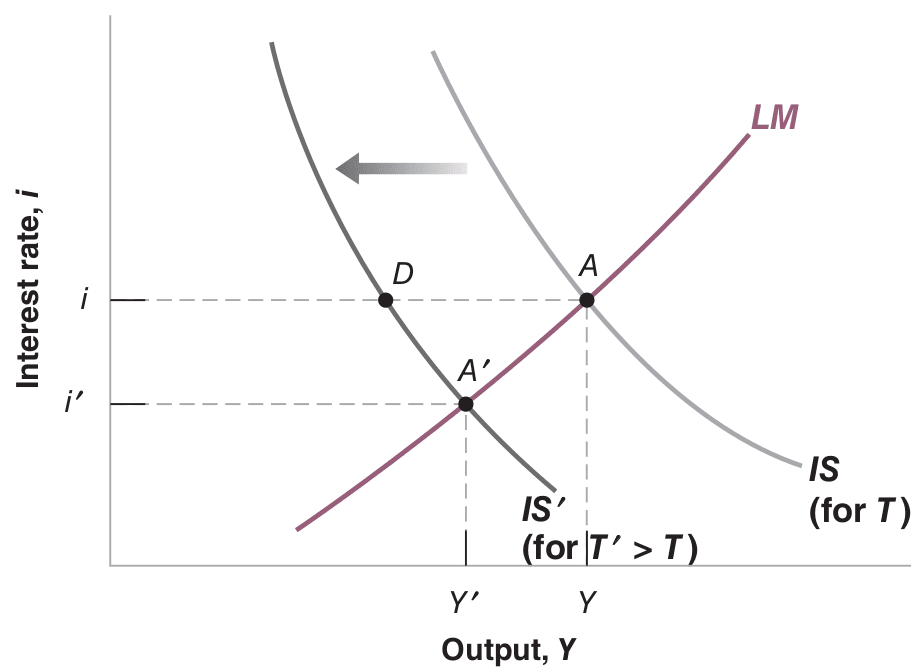

26.2.0.1 Fiscal Policy

Fiscal contraction or consolidation refers to fiscal policy that reduces the budget deficit; increasing the deficit is called a fiscal expansion. Taxes and government spending affect the IS curve but not the LM curve, whereas changes in money supply impact the LM curve but not the IS curve. Figure 26.3 provides an overview of fiscal and monetary policy effects in the IS-LM model.

Note: Blanchard & Johnson (2013, p. 98)

When answering questions about the effects of policy changes, follow these three steps:

Equilibrium Impact:Determine how the change affects equilibrium in the goods market and the financial markets. Specifically, assess how it shifts the IS and/or the LM curves.

Intersection Effects: Characterize the effects of these shifts on the intersection of the IS and LM curves. Analyze what this does to equilibrium output and the equilibrium interest rate.

Descriptive Analysis: Describe the effects in words.

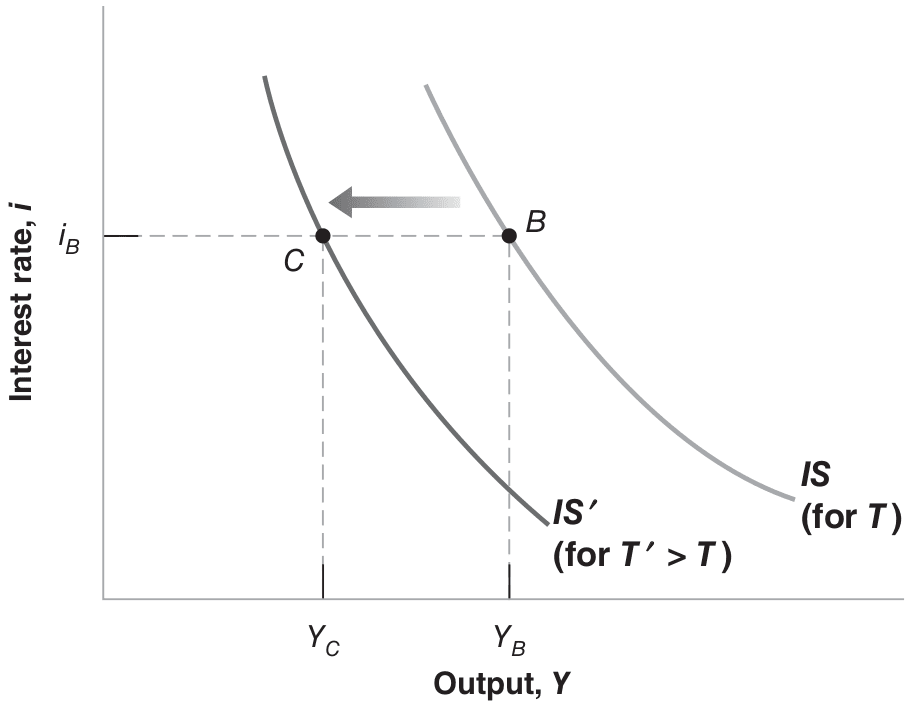

1. Impact on output:

Note: Blanchard & Johnson (2013, p. 95)

Impact on financial markets:

Note: Blanchard & Johnson (2013, p. 95)

2. Overall Effects:

Note: Blanchard & Johnson (2013, p. 95)

3. In Words: An increase in taxes leads to lower disposable income, causing people to reduce consumption. This decrease in demand, in turn, leads to a drop in output and income. Simultaneously, lower income reduces money demand, lowering the interest rate. The interest rate decline mitigates but does not fully counteract the increased tax impact on goods demand.

- Effects of a Monetary Expansion

A monetary expansion results in higher output and a lower interest rate.

Note: Blanchard & Johnson (2013, p. 97)

26.3 Limitations of the IS-LM model

- It’s built on simplistic and unrealistic assumptions about the macroeconomy. Sir John Richard Hicks (1904-1989)1 claimed the model’s flaws were fatal, better used as a “classroom gadget, to be superseded by something better.” However, new or optimized IS-LM frameworks have emerged over time.

- The model’s a limited policy tool; it doesn’t detail how tax or spending policies should be formulated, limiting its practical appeal.

- It lacks insights on inflation, rational expectations, or international markets, though later models attempt to incorporate these. The model also overlooks capital formation and labor productivity.

Exercise 26.2 Rap battle

Source: Youtube

Watch the video of Figure 26.8 and read the lyrics and comments at Genius Lyrics. Access comments on shaded text.

Explain the Keynesian strategy for combating bust and boom cycles. Explain Friedrich Hayek and the Austrian school’s approach to fighting bust-and-boom cycles. Also consider the video screenshots in Figure 26.9.

Source: Youtube

British economist and major twentieth-century figure. See: John Hicks↩︎